Families searching for care solutions for an elderly couple in 2025 face a surprising dilemma: the sticker price for a live-in caregiver has soared, but knowing all the real numbers—and how to pay less—can transform what seems impossible into your smartest move yet.

What You’re Really Paying For: The True Breakdown of Live-In Caregiver Costs in 2025

You may have seen ads for ‘affordable home care,’ but when it comes to full-time, live-in care for an elderly couple, the numbers quickly add up. Unlike hourly caregivers, live-in professionals provide round-the-clock help: cooking, mobility transfers, managing chronic conditions, midnight bathroom trips, and companionship for two adults. Every extra need—like dementia care or special mobility help—bumps the price higher.

Price Anchoring Alert: The national average for live-in care in 2025 ranges from $6,500 to $12,000 per month for a couple, according to leading agencies and industry trackers. In high-cost states (California, New York), expect to pay the upper end or even more.[1][2][3][7]

- Direct hire (no agency): $6,500–$9,000/month

- Via agency: $8,500–$12,000/month (agencies handle payroll, taxes, replacement care)

- 24/7 ‘awake’ care (multiple aides): $15,000–$22,000/month—much higher, but sometimes medically necessary[1][5][9]

These numbers include the caregiver’s base salary (for both adults), but that’s only the start. Let’s break down the real costs line by line:

All the Hidden Extras: What the Bill Really Covers

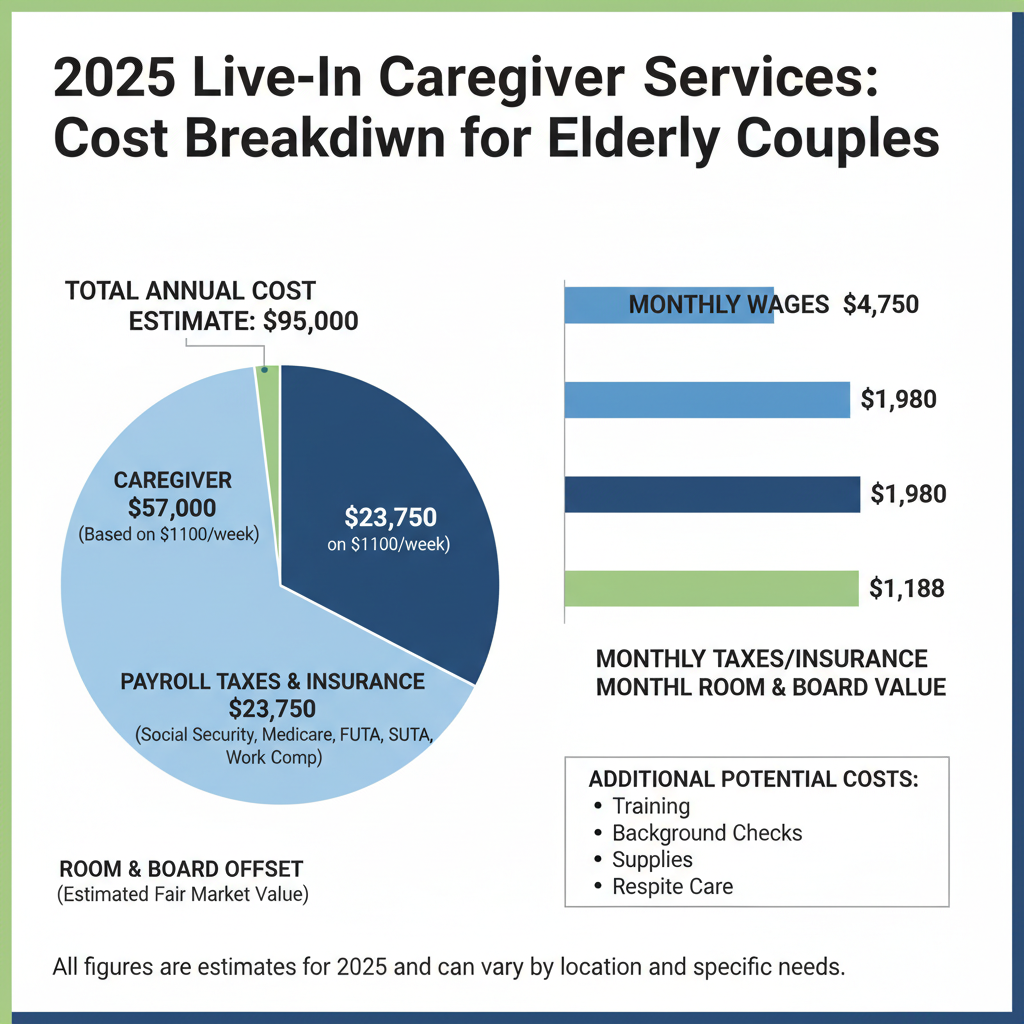

- Room & Board: You must provide a private room and cover basic groceries/utilities for your caregiver. Estimate $450–$750/month on top of their wage.

- Payroll Taxes (if you hire directly): Add 7.65%–15% for Social Security, Medicare, unemployment, and possibly workers’ comp (about $500–$1,000/month).

- Overtime Pay: Many states require you to pay overtime if your caregiver works more than 40 hours/week. Agencies usually build this into their rate; direct hires often need special schedules to avoid legal trouble.

- Backup/Emergency Care: Budget for temp replacements (often at premium rates) if your primary caregiver gets sick or takes vacation.

- Insurance: Most agencies include liability and bonding insurance in their markup. If hiring privately, consider separate liability insurance (typically $30–$50/month).

Live-In Care vs. Assisted Living and 24-Hour Home Care: The 2025 Showdown

| Option | 2025 Monthly Cost | What’s Included | Pros | Cons |

|---|---|---|---|---|

| Live-In Caregiver (Couple) | $6,500–$12,000 | Personalized care, one-to-one, in your home | Privacy, flexibility, continuity | Higher cost than assisted living, hiring/management hassle |

| Assisted Living Facility | $5,900–$8,000 (per unit, may charge extra per person) | Group setting, activities, meals, some nursing | All-inclusive, social | Less personal attention, less privacy, can separate couples |

| 24-Hour ‘Awake’ Home Care | $15,000–$22,000 | Multiple aides, no one sleeps on shift | Best for severe needs, safest | Prohibitively expensive for most families |

Urgency: Inflation and a nationwide caregiver shortage are driving prices up 5–10% year over year. Waiting could cost thousands more.

Who’s Really Hiring in 2025? Popular Agencies & Current Products

- Home Instead Senior Care: Live-in care plans, typically $8,500–$11,000/month for couples in major metros. 24/7 support and replacement guarantees.

- BrightStar Care: High-acuity care, charges $9,000–$14,000/month for couples with advanced medical needs.

- Care.com Direct Hire: Find private caregivers. Typical rates: $225–$350/day (plus taxes, insurance, backup care not included).

- Right at Home: Custom plans for couples. Flat-rate live-in packages starting around $7,200/month, rising with complexity and overnight vigilance needs.

- Honor Home Care: Tech-enabled scheduling, $9,000–$12,000/month for couples, includes most payroll/tax handling.

Expert opinion: Agencies charge more, but reduce the risk of last-minute gaps and take care of taxes, worker’s comp, and liability insurance—critical for peace of mind.

How to Pay Less (or Get Help Affording It)

Don’t let sticker shock stop you: Even with five-figure annual costs, families are getting creative—and getting help. Here’s how to maximize your options:

- Long-Term Care Insurance: If you or your loved one have a policy, now’s the time to use it. Policies written before 2020 are especially valuable (newer ones have stricter caps). Always check if policies cover both spouses in the home.

- Medicaid Home & Community Based Services (HCBS): In some states, Medicaid will help pay for live-in or 24-hour care if both spouses qualify financially and medically. This is changing fast—apply ASAP to avoid long waitlists.

- Veterans Benefits: If either spouse is a veteran, look into the VA Aid & Attendance Pension, which can add $2,600+/month for a couple toward in-home care.

- Flexible Spending Accounts and Health Savings Accounts (FSAs/HSAs): Some eligible costs can be paid from these tax-advantaged accounts.

- Reverse Mortgages: Homeowners aged 62+ can tap home equity for care funding without selling the house. Consult a HUD-approved counselor first.

- State & Nonprofit Grants: Many states and charities (like the Alzheimer’s Association) offer temporary caregiver relief grants—application windows fill fast.

Pro Tip: Some agencies now offer “partial live-in” or “split shift” packages to lower costs—great for couples who only need night help or a few wake-up calls per day.

Action Plan: Steps to Secure the Right Care for the Right Price

- Get a detailed needs assessment from a certified geriatric care manager or your local Area Agency on Aging. List all ADLs (activities of daily living), medical needs, and preferred schedules.

- Interview multiple agencies and private caregivers. Demand a written, itemized cost breakdown and clarify backup coverage for illness or emergencies.

- Ask for references and check reviews—sites like Care.com and Trustpilot post real client feedback.

- Review all insurance, benefit, and aid options—some require lengthy approval, so start paperwork now.

- Negotiate: Agencies may waive setup fees, add free backup days, or discount for paying several months in advance. Don’t be shy!

Ready to Take Control? Don’t Wait—Caregiver Costs Will Only Climb!

If you’re considering live-in care for an elderly couple, get the conversation started today. Talk to a senior care specialist, get a written quote, and check your insurance—before costs jump again. Demand transparency, ask about every line item, and use every benefit and program you can. The difference can be thousands per year—and better quality of life for those you love.

Want a personal cost estimate, a list of local agencies, or a step-by-step financial aid guide for your state? Reach out to a certified senior care advisor now—slots are limited as demand skyrockets in 2025!