Choosing a senior community with on‑site healthcare can feel like signing a blank check, but once you unpack the fee structure, it becomes a predictable—sometimes even cost‑saving—strategy instead of a financial gamble. The key is understanding exactly what you’re paying for, how care is billed, and how that compares to staying at home plus private care over 5–10 years.

What You’re Really Paying For

Every senior community with on‑site healthcare essentially sells three things wrapped together: housing, hospitality (meals, housekeeping, activities), and healthcare access (nursing, therapy, clinics, and emergency response). Communities differ less on whether they offer these pieces and more on how they slice and price them—flat fees, tiered care packages, or pay‑as‑you‑go clinical billing. Understanding that structure is the first step to avoiding surprise bills and choosing a community that matches your real risk profile rather than your best‑case scenario.

Entrance Fee vs. Rental: Two Very Different Bets

Most full‑service communities with on‑site healthcare fall into two buckets: Continuing Care Retirement Communities (CCRCs, also called Life Plan Communities) that charge a large entrance fee, and rental communities that charge month‑to‑month with little or no upfront buy‑in. CCRCs may require entrance fees from under $100,000 to well over $500,000 in higher‑end markets, often with partial refund options if you move out or pass away within a set period, while rentals typically ask only for a community fee ranging from roughly one to three months’ rent. That upfront difference is the clearest price‑anchoring moment—families often fixate on the six‑figure entrance fee and ignore the long‑term tradeoff in monthly costs and included care.

Housing vs. Care: What’s Included?

In most rental assisted living settings, the base monthly fee covers housing, basic utilities, meals, housekeeping, activities, and limited help with daily tasks; additional care, such as increased assistance with bathing, transfers, or medication management, is tiered into higher monthly levels as needs grow. By contrast, many CCRCs bundle certain levels of healthcare into the contract, allowing residents to move between independent living, assisted living, and sometimes short stints in skilled nursing with predictable or discounted rates relative to the open market. The practical question is not “Is care available?” but “Which care is already pre‑paid and which will trigger add‑on charges later?”

How On‑Site Healthcare Is Billed

On‑site healthcare in senior communities usually comes in three flavors: daily support from the community care team, services from an on‑site clinic or medical practice, and separately billed therapy or home health services. Families often assume everything that happens inside the building is included in the monthly fee; in reality, different providers inside the same campus can bill separately under their own Medicare and insurance agreements. The more you understand these boundaries up front, the less you risk getting blindsided by stacked copays and coinsurance.

Daily Support and Care Packages

Most assisted living or memory care units on a campus charge for daily support using either care levels (e.g., Level 1–5) or a point system that translates individual tasks into a monthly fee. Communities may start with a base monthly rate for housing and hospitality and then add $500–$2,500+ per month for higher care levels as needs increase. This means that what begins as a relatively affordable assisted living stay can gradually approach or even exceed the cost of a nursing home when intensive hands‑on support is needed daily.

On‑Site Clinics and Medicare Billing

Many higher‑end communities now host on‑site primary care clinics, geriatric practices, or concierge‑style medical groups that bill Medicare, Medicare Advantage, or commercial insurance directly rather than through your monthly community bill. These clinics may charge standard office visit copays under your plan, but can save significant money and hassle by reducing hospital transfers, ER visits, and ride costs for off‑site appointments. Some communities also partner with in‑house home health and therapy providers, meaning services like physical therapy or wound care are billed as separate healthcare claims even though they occur just down the hall from your apartment.

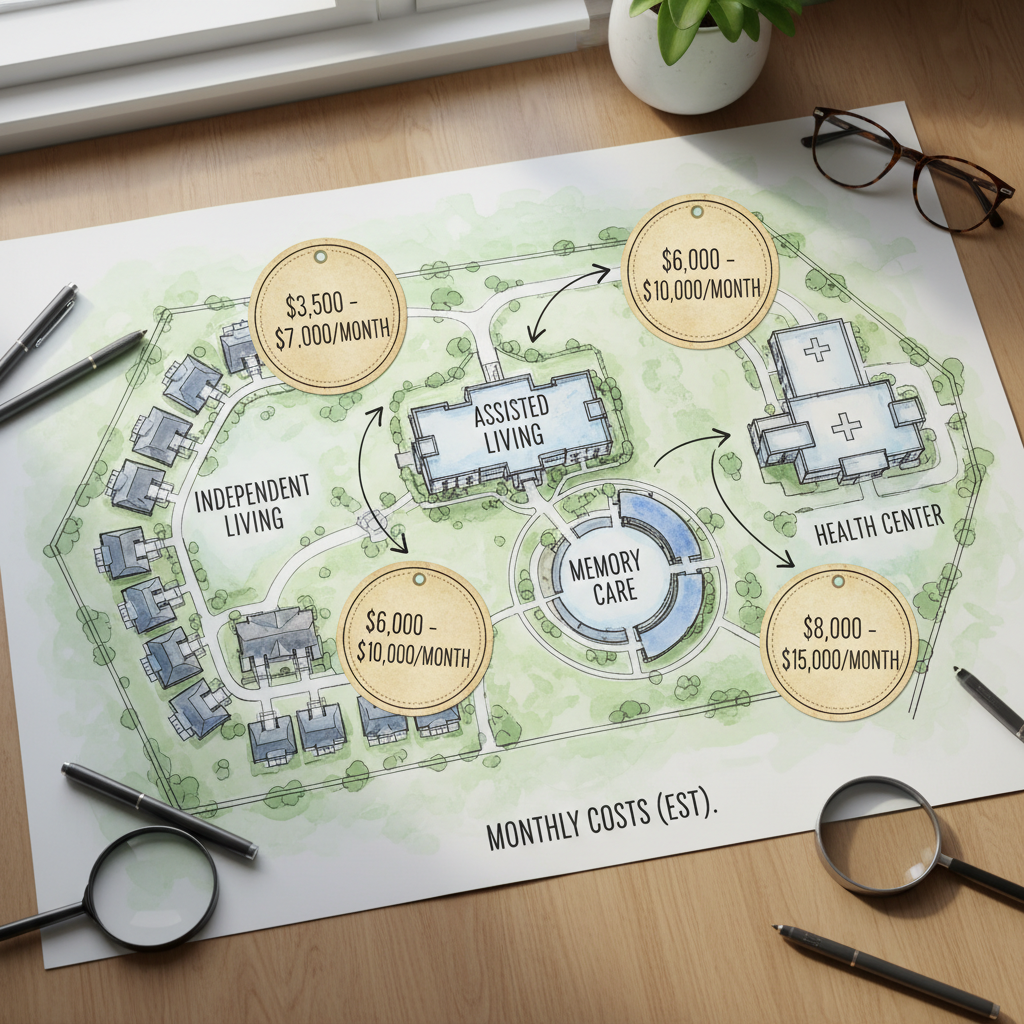

Current Cost Benchmarks and What They Mean

To make sense of the numbers on marketing brochures, it helps to anchor your expectations with typical national medians and then adjust for your local market. Nationwide, independent living communities often price in the low‑to‑mid‑$3,000s per month for rent plus services, while assisted living averages closer to the mid‑$5,000s per month and memory care can run significantly higher. Skilled nursing for 24/7 medical supervision can easily climb into the high‑$8,000s to $10,000+ per month range for semi‑private or private rooms, which is where the “insurance” value of a CCRC contract starts to matter.

Sample Budget: Community vs. Staying at Home

Consider a scenario where a parent needs moderate help with daily activities but not full nursing care: at home, you might pay $30–$35 per hour for a home health aide, which at just six hours a day can approach or exceed $5,000 per month before housing, food, utilities, transportation, and home maintenance. A mid‑market assisted living apartment with on‑site healthcare access might charge around $5,500–$6,500 per month for rent, meals, basic care, and activity programming, with add‑on fees as needs climb. Over a multi‑year horizon, the home‑care path might look cheaper in year one but become more expensive or logistically fragile as hours and complexity ramp up.

| Option | Housing & Living Costs (Monthly) | Care Costs (Monthly) | Pros | Cons |

|---|---|---|---|---|

| Stay at home + part‑time aide | $2,000–$3,500 (mortgage, taxes, utilities, food, transport) | $3,000–$6,000 (home health aide hours) | Familiar environment, flexible hours, can scale gradually | Care coordination burden, home may need expensive modifications, risk if caregiver cancels |

| Rental assisted living with on‑site healthcare | $4,500–$6,500 (apartment, meals, services) | $500–$2,500 (care level fees, therapies billed separately) | Built‑in safety net, predictable routines, quick access to help | Care costs rise as needs increase, less flexibility on providers |

| CCRC with entrance fee | $3,500–$6,000 (monthly service fee) | Discounted or partially included as care level increases | Priority access to higher levels of care, more predictable long‑term costs | High upfront entrance fee, complex contracts, not ideal for short stays |

Where Medicare, Medicaid, and Advantage Plans Fit In

One of the most misunderstood parts of on‑site healthcare is the role of public and private insurance: these programs pay for medical care, not for rent, meals, or most personal care. Medicare and Medicare Advantage plans can help with short‑term skilled nursing, rehab, home health, and clinic visits, but they do not cover long‑term custodial care or room and board in senior communities. Medicaid, where available, can sometimes offset assisted living or memory care services through waivers, yet coverage is state‑specific, capacity‑limited, and often excludes the housing portion of your bill.

Medicare Advantage and On‑Site Care

Some communities now market special partnerships with Medicare Advantage or other managed care plans that emphasize care coordination, telehealth, and in‑community primary care. These arrangements can reduce hospitalizations and out‑of‑pocket costs for medical episodes, but they rarely change the underlying rent and service structure of the community; they mainly affect how doctor visits, tests, and therapies are paid for and what copays you face. When comparing communities, it is crucial to ask whether the on‑site providers are in‑network with your parent’s existing plan, or whether switching plans would be advantageous to fully use the on‑site clinic and therapy services.

New Trends That Affect Your Wallet

Operators are increasingly moving toward value‑based healthcare partnerships, where they are rewarded for keeping residents healthier and out of the hospital—something that often benefits both families and insurers financially. At the same time, rising labor, insurance, and compliance costs are pushing monthly rates and care surcharges higher, and some states are tightening Medicaid reimbursement, making purely public‑pay options harder to find. The net result is more pressure on private‑pay families to understand contracts, shop carefully, and negotiate where possible rather than assuming prices are fixed.

Hybrid and Tech‑Enabled Care Models

Some communities now combine traditional assisted living or independent living with in‑house telehealth hubs, remote monitoring, and nurse practitioner‑led clinics, effectively turning the building into an outpatient ecosystem. While this can carry a modest tech or concierge fee, it may reduce costly emergency visits and outside transportation, an important hidden savings when comparing to staying at home. A growing number of campuses also offer flexible, à‑la‑carte personal care services, blending independent living pricing with targeted add‑on care so residents only pay for what they actually use.

How to Read the Fine Print (and Push Back)

Because contracts are dense, it helps to approach the selection process like a business negotiation rather than a purely emotional decision. You can often negotiate move‑in fees, ask for rate‑lock periods, or request written caps on annual increases to protect against aggressive future hikes. When communities know you are comparing them side‑by‑side—including the projected 5‑ to 10‑year cost of rising care levels—they are more likely to be flexible with incentives to win your business.

Step‑by‑Step Cost Vetting Checklist

First, request a breakdown that separates housing, hospitality, and care charges, then ask how those amounts have increased over the last five years. Second, have the community model three scenarios—a light‑care year, a moderate‑care year, and a heavy‑care year—so you see your possible monthly range instead of a single attractive starting rate. Third, share the contract and pricing grids with a financial planner or elder law attorney to confirm how the entrance fee or monthly charges fit into your broader assets, tax picture, and estate goals.

When Does a Community With On‑Site Healthcare Make Financial Sense?

A community with robust on‑site healthcare is most financially compelling when you expect needs to rise, want to cap risk, and value the convenience of a single, coordinated setting over juggling multiple outside providers. If your parent is very healthy with limited assets and a strong family caregiving network nearby, it may be more cost‑effective to remain at home for a time and delay a move until care needs spike. But if they live alone, already need several hours of help daily, or are at high risk of hospitalization, the bundled safety net of a community with on‑site healthcare often becomes the less risky, more predictable path.

Your Next Three Action Steps

To move from anxiety to clarity, start by gathering actual price sheets and care level grids from three local communities that offer on‑site healthcare, plus estimates for home‑based care hours you would realistically need. Then, build a side‑by‑side five‑year cost projection using conservative assumptions about rate increases and gradually higher care needs, treating your entrance fee or deposits as part of a long‑term insurance strategy rather than a simple purchase. Finally, bring those projections to a family meeting and, if possible, a financial planner, so you can decide not just which option feels safest emotionally but which actually protects savings and reduces the odds of future financial shocks.