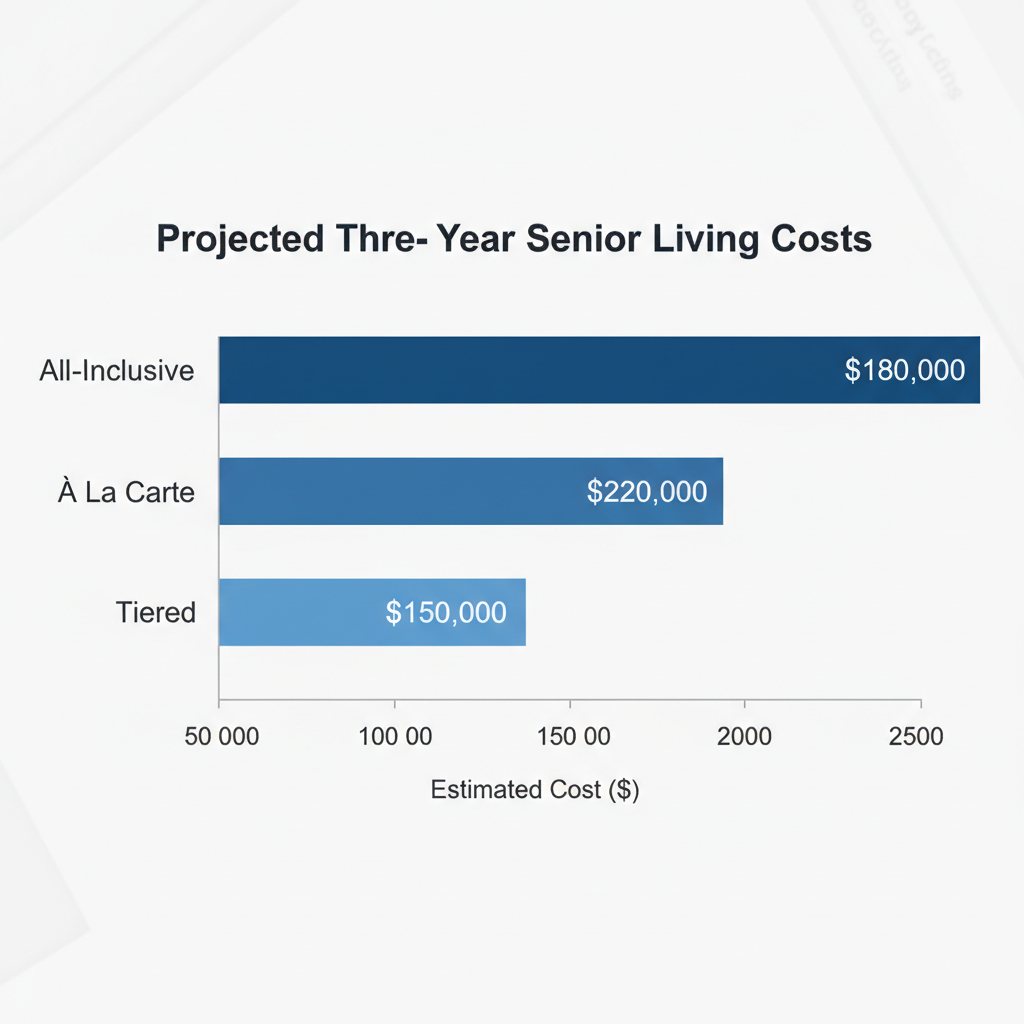

What if a single detail in your senior living contract could save—or cost—you thousands each year? Most families get hit with bill shock not from the base price, but from hidden escalators baked into the pricing model itself. In 2025, senior living communities have gone beyond simple rent: you now face a maze of all-inclusive, à la carte, and tiered pricing models—each with its own financial landmines and deal-making opportunities.

Smarter Choices: Why Pricing Model Matters More Than the Sticker Price

Think you can just hunt for the lowest monthly rate? Think again. The real cost (and risk) is how your bill grows over time as your needs change. Here’s why each model is trending in 2025—and who stands to win or lose with each choice.

All-Inclusive: Predictability—But at a Premium

With all-inclusive pricing, one monthly payment covers nearly everything: housing, meals, housekeeping, basic assistance, and scheduled activities. In 2025, the national average for all-inclusive independent living is $3,065/month, while assisted living hovers near $5,900/month (e.g., Sunrise Senior Living, Holiday by Atria)[1][3][6]. The big advantage? Your bill is stable even if you occasionally need more support. But beware: you may overpay if you require few extra services, and some amenities (like salon visits or private transport) are often still extra[3][4].

Sample 2025 Bill (All-Inclusive, Assisted Living):

- Base rent: $5,900

- Added medical transport: $0 (included)

- Medication management: $0 (included)

- Total predictable monthly cost: $5,900

Best For: Seniors with moderate or increasing care needs, or those who value absolute predictability over potential savings.

Hidden Traps: Some communities exclude expensive services. Always get a written list of exclusions before signing[3].

À La Carte: Low Entry, But Watch for Creep

The à la carte (fee-for-service) model charges a lower base rent ($2,250–$3,500/month for independent living, $4,500–$7,000/month for assisted)[1][3][7]. You pay only for the specific services you use, like bathing help, medication reminders, or meal delivery. Brands like Brookdale and Senior Lifestyle often use this model for flexibility.

Sample 2025 Bill (À La Carte, Assisted Living):

- Base rent: $4,500

- Bathing assistance (4x/month): $250

- Medication management: $180

- Housekeeping add-on: $120

- Total monthly cost: $5,050

Best For: Highly independent seniors who rarely need extra help and want the lowest baseline cost.

Hidden Traps: If your needs increase, bills can skyrocket—sometimes exceeding all-inclusive rates by year two or three[3][4][5]. Rate increases for added care are often higher than the initial rent hikes.

Tiered Pricing: Pay for the Care Level You Need—But Risk Sudden Jumps

With tiered pricing, your monthly rate depends on your assessed level of care (e.g., basic, moderate, extensive). Each tier unlocks a bundle of services, and you’re re-assessed 2–4 times a year. National averages for 2025:

- Tier 1 (Basic): $4,800/month

- Tier 2 (Moderate): $5,800/month

- Tier 3 (Advanced): $7,200/month

Many Life Plan and CCRC communities (like Erickson Senior Living, Acts Retirement-Life Communities) use this model[1][5].

Sample 2025 Bill (Tiered, Assisted Living):

- Base rate (Tier 1): $4,800

- Move to Tier 2 after 6 months: $5,800

- Annual increase: 5–7%

Best For: Seniors whose care needs may grow gradually; those who value aging in place with transparent care escalation.

Hidden Traps: Tier jumps can be abrupt (a $1,000/month hike is common). Assessments are often triggered by small changes (e.g., new medication), so costs may rise with little warning[3][4][5].

Real-World Cases: Which Model Saves the Most in 2025?

A comparative three-year projection shows:

- À la carte is cheapest if you remain healthy and independent—but risks the highest bills if care needs increase.

- All-inclusive becomes the best value for those needing stable, ongoing support, since rates are locked even as you use more services.

- Tiered offers a middle ground, but sudden care escalations (after a hospital stay, for example) can quickly erode savings.

Recent trend: As of mid-2025, independent living communities are raising initial rates faster (up 16.9% year-over-year) than assisted or memory care, but offering larger move-in discounts and rent freezes to entice new residents[2]. Some operators now use dynamic pricing—similar to airlines—to offer deals or fill units quickly, so timing your move can save thousands[1][2].

Hidden Fees & Negotiation Power Plays

Here are the most common 2025 fees—and how to fight them:

- Community/Entrance Fees: Life Plan and CCRC entry fees range from $40,000–$2 million (partially refundable). Rental models often have $1,000–$5,000 move-in fees[1][5].

- Annual Rate Increases: Expect 5–8% annual increases, but some all-inclusive contracts allow you to lock rates for multiple years—if you ask!

- Care Assessment Fees: Tiered and à la carte models may charge $200–$500 for each level-of-care evaluation.

- Optional Services: Salon, private transport, and guest meals are rarely included (“a la carte” even in all-inclusive communities).

- Negotiation Tip: Ask for current move-in incentives: rent freezes, waived fees, or bundled care packages. Operators often have unpublished deals, especially in slower seasons[1][2][3].

Five Steps to Slash Your Senior Living Bill in 2025

- Request a detailed itemized quote—insist on seeing every included and extra charge, line by line.

- Time your move strategically—move-in specials are most generous in winter and early spring.

- Negotiate multi-year rent freezes—especially if paying a premium for all-inclusive models.

- Review your care plan quarterly—eliminate unused services or downgrade tiers if health improves.

- Shop competing communities—and use competitor discounts/offers as leverage at your preferred location[1][2][3][5].

Don’t Settle—Command Better Pricing

Senior living in 2025 is more flexible, negotiable, and data-driven than ever before. Families who understand the differences between all-inclusive, à la carte, and tiered pricing models don’t just save money—they avoid the “gotcha” fees that drain retirement savings.

Ready to take charge? Download a side-by-side comparison worksheet, schedule in-person tours during promotional periods, and ask every community: “What’s your best deal right now, and what will my monthly bill look like if my needs change next year?” You’ll join the savvy minority who lock in lasting value—while others pay the real price of confusion.

Act now: Communities adjust rates quarterly, and the steepest discounts are often unpublished. Don’t wait—secure your spot while the best deals last!