Thinking about veneers but worried the price will crush your smile before you even get to the chair? You’re not alone. In 2025, veneers are more popular than ever for transforming smiles—yet the cost, which can range from $900 to $3,500 per tooth[2], still feels out of reach for many. Here’s the game-changer: today’s best dentists don’t just offer veneers—they help you finance them smartly, using a toolkit of options that can fit nearly any budget. There’s no need to wait or settle for less—here’s your step-by-step roadmap to afford veneers confidently, without hidden traps or surprise bills.

Step 1: Know Your Veneer Costs—And Why They Vary

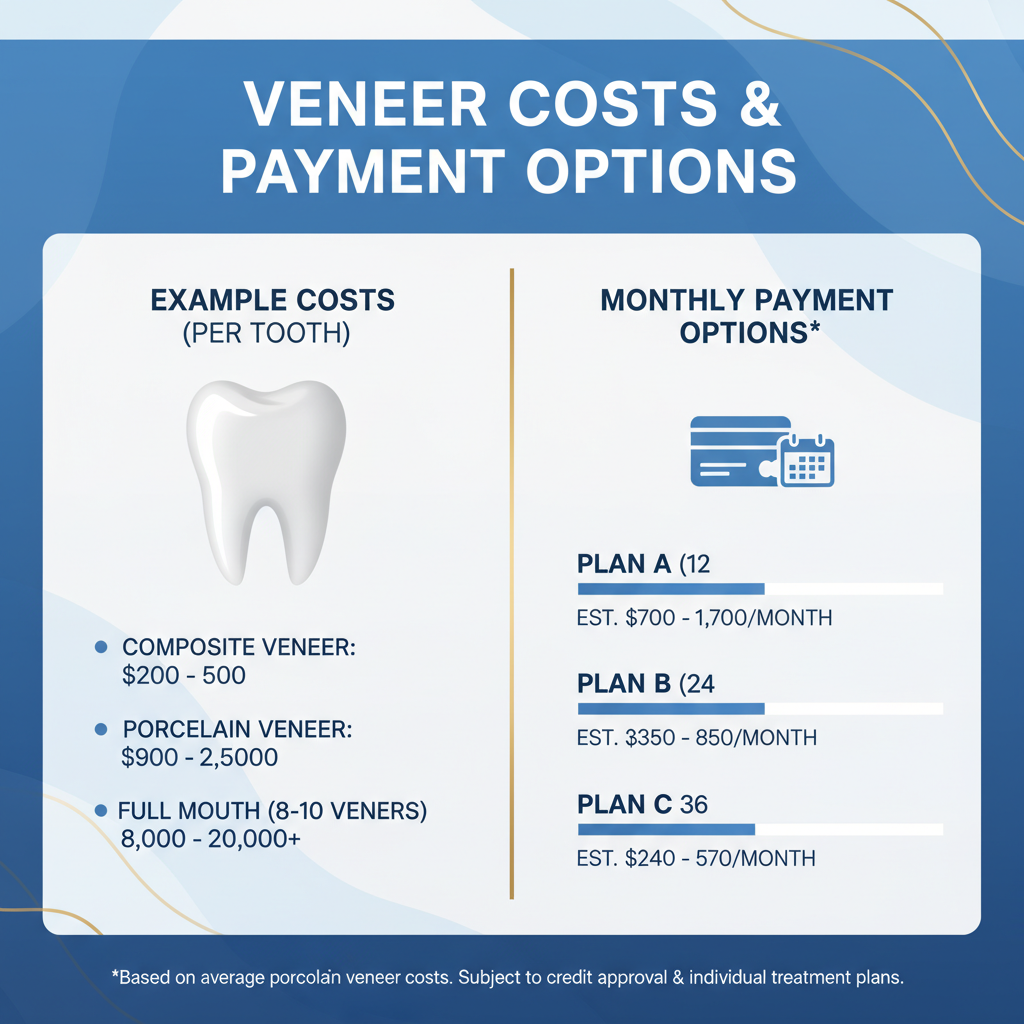

Porcelain veneers (the gold standard) typically run $900–$3,500 per tooth, while composite veneers can start as low as $250 and top out around $1,500[2][3]. The final quote depends on:

- How many teeth you’re treating

- Type and brand of veneer material

- Your dentist’s experience and location

- Additional work needed (whitening, contouring, etc.)

Pro tip: many practices bundle services as “Smile Packages” for multi-tooth cases, dropping the per-tooth price and maximizing value[1].

Step 2: Leverage In-House Payment Plans—Often the Easiest Start

Lots of reputable dentists now offer in-house payment plans—simple, custom monthly payments managed directly by the office, often without a third-party lender[3][4][10]. Here’s how it usually works:

- Small or zero down payment

- No (or low) interest if paid within 6–12 months

- Quick, easy approval—often with no hard credit check

Example: For a $6,000 smile makeover (6 porcelain veneers), an in-house plan might offer $500/mo for 12 months, 0% APR if paid on time.

Who qualifies? In-house plans are more accessible for fair-to-good credit (score 600+), but some offices work with lower scores—ask upfront. Check for transparent terms—avoid plans with balloon payments or hidden fees.

Step 3: Explore 0% Promotional Financing & Buy Now, Pay Later (BNPL)

Third-party healthcare lenders have revolutionized dental financing. Examples include:

- CareCredit®: 0% APR for 6–24 months; longer terms (up to 60 months) with competitive fixed rates[3][4][7]. Fast approval, but watch for deferred interest clauses if not paid in time.

- Cherry®: Soft credit check (no impact on score), instant approval, 0–30% APR, and flexible 3–60 month terms[4][8]. Over 80% approval rates—even for modest credit. Funding up to $50,000.

- Smile Generation® Financing Marketplace: Up to $75,000 for dental care, 0% APR on approved credit, up to 144-month terms, and soft credit checks[5].

Example monthly payments:

- CareCredit: $8,000 in veneers at 0% for 24 months = ~$334/month

- Cherry: $12,000 full-mouth case at 6.99% for 60 months = ~$237/month

BNPL providers like Cherry can approve those with weaker credit (as low as 580), but rates may be higher. Always confirm the total repayment amount before signing.

Step 4: Use Healthcare Credit Cards, HSAs, and FSAs—Don’t Miss Tax Savings

- Healthcare credit cards (CareCredit, Wells Fargo Health Advantage): Ideal if you can pay in full during the 0% period.

- Health Savings Accounts (HSAs) & Flexible Spending Accounts (FSAs): Both allow you to pay for veneers pre-tax, saving up to 30% depending on your tax bracket[2]. HSAs roll over every year, FSAs usually have a “use it or lose it” rule.

Action: Ask your dentist for an itemized estimate—submit this to your HSA/FSA administrator to reimburse yourself or pay directly.

Step 5: Personal Loans—When to Consider (and When to Avoid)

Medical loan providers like LendingClub or LightStream offer personal loans for larger cases ($5,000+). These may be right if:

- Your credit is strong (score 660+ for best rates)

- You want a longer payoff window (up to 7 years)

- You prefer a fixed monthly payment and no revolving debt

But: Interest rates can start at 8–15% and climb much higher if your credit is less than perfect[4]. Origination fees and variable interest mean you must check the fine print.

Step 6: Staged Treatment—Affordable, Step-by-Step Smile Upgrades

Can’t swing the full price upfront? Many dentists will break your treatment into staged phases: start with your most visible teeth (like four uppers), then add more over 6–12 months as your budget allows. This lets you:

- Spread out payments, reducing monthly costs

- Take advantage of multiple yearly FSA/HSA cycles

- See results quickly and build confidence

Social Proof Alert: Many patients share success stories of starting with two or four veneers and gradually building their dream smile—a trend rising in 2025[3].

Expert Tips: Avoiding Predatory Terms & Maximizing Value

- Always check APR after the promo period—some lenders retroactively charge high interest if not paid off on time.

- Compare total cost, not just monthly payments. A longer term often means you’ll pay more overall.

- Ask about bundled discounts for multiple veneers or “Smile Packages”—some practices knock off 10–20% with a larger case[1][3].

- Use dental discount plans (like Gentle Dentistry’s annual memberships) to save 10–20% on cosmetic procedures for a low annual fee[10][3].

Turn Interest Into Action: Your Next Steps

1. Book a veneer consultation at a reputable cosmetic dentist—ask for a cost estimate and all financing options in writing.

2. Compare in-house and third-party plans—don’t be shy about negotiating terms or monthly payments.

3. Maximize your savings by timing staged treatment with FSA/HSA cycles or seeking bundled deals.

4. Ready to get started? Apply for pre-approval with CareCredit or Cherry online—it won’t impact your credit in most cases, and you’ll know exactly what you can afford before you ever sit in the chair.

Don’t let sticker shock steal your smile. With today’s financing options, dream veneers are more accessible than ever—if you know where to look, which questions to ask, and how to avoid costly pitfalls.