If you’re staring down the barrel of a major dental bill—braces for your teen, an implant for yourself, or a mouthful of crowns—the stakes are high. Pick the wrong insurance, and you could pay thousands more than you have to. But compare the right way, and you’ll lock in coverage that actually pays when it matters most. Here’s a step-by-step, outcome-driven guide for comparing dental insurance quotes online when you know major work is in your future.

Why Most People Overpay (or Get Burned) on Major Dental Work

Dental insurance isn’t built for big claims. Most plans are designed to cover preventive care and basic fillings, not four-figure procedures. That’s why it’s essential to look past low premiums and focus on what the plan actually pays for crowns, implants, or orthodontics.

The Truth About Coverage Tiers

- Preventive: Nearly every plan pays 100% for checkups and cleanings.

- Basic: Fillings and simple extractions—usually covered at 70% to 80%.

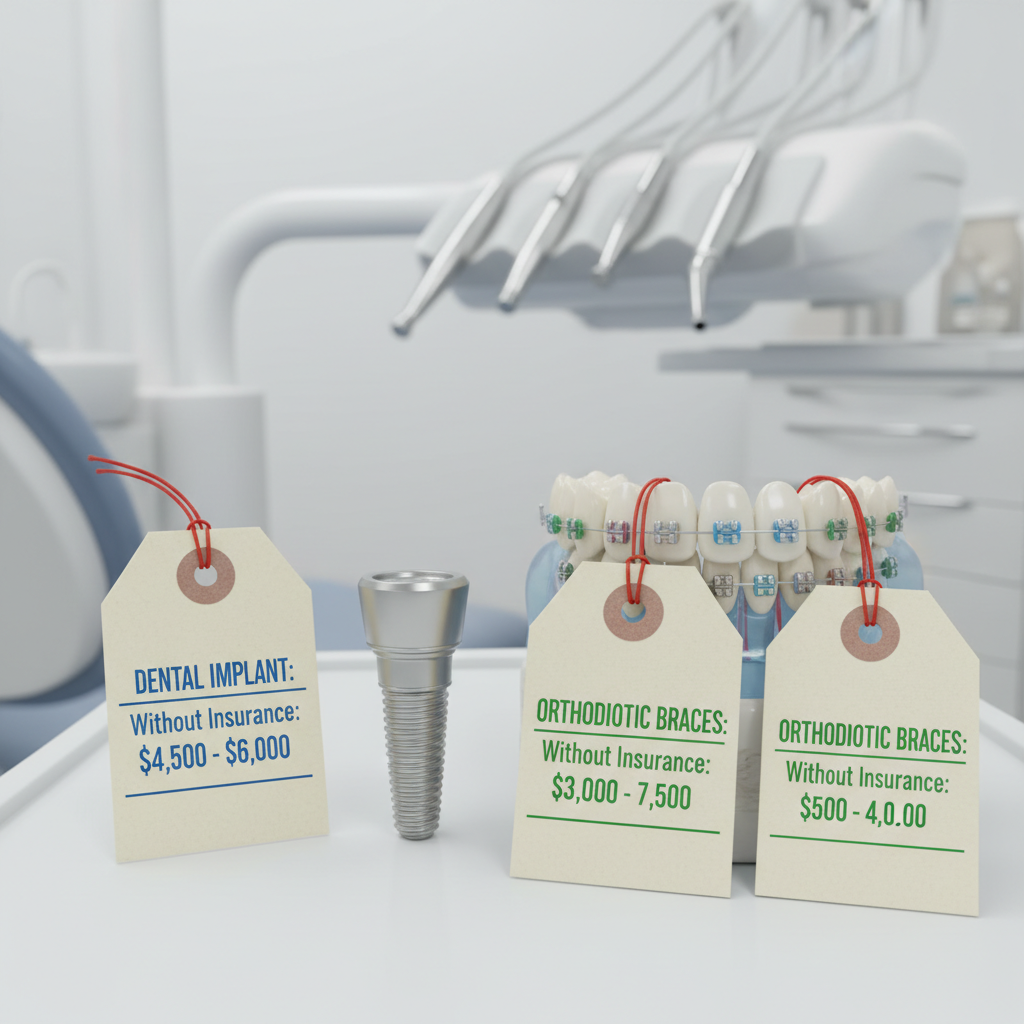

- Major: Crowns, bridges, dentures, implants, orthodontics—typically covered at 40% to 50%, and sometimes not at all for implants or adult braces.[1][3][5]

Step 1: Zero In on Plans That Cover What You Need

Most comparison sites (like Cigna, Delta Dental, and Spirit Dental) let you filter or compare plans based on coverage for key procedures. Here’s how to use them so you don’t waste time on plans that won’t help:

- Check for implants and orthodontics: Many plans exclude these, or only cover them for kids. Look for “Implant Coverage” or “Ortho Add-On.”

- Waiting periods: If you need work soon, skip plans with 6-12 month waits for major services. Spirit Dental and Anthem’s HMO plans have no waiting period.[1][2]

- Annual and lifetime maximums: For major work, you want the highest annual maximum you can afford. Plans like Spirit Dental offer up to $5,000/year—most competitors cap out at $1,500-$2,000.[1][3]

Current Standout Plans for Major Dental Work (2025)

| Plan | Major Work Coverage | Ortho/Implant Coverage | Waiting Period | Annual Max | Monthly Price |

|---|---|---|---|---|---|

| Spirit Dental & Vision | 50% | Both covered | None | $5,000 | $40-$90 |

| Delta Dental PPO | 50% | Ortho add-on, Implants on select plans | 6-12 months | $1,000-$2,000 | $45-$85 |

| Cigna Dental 1500 | 50% | Ortho included (12 months wait) | 12 months | $1,500 | $35-$75 |

| Anthem Dental HMO | Copays (fixed fees) | Some implant/ortho on select networks | None | No max | $20-$45 |

Step 2: Dig Into the Fine Print—What to Check Before You Buy

- Exclusions: Read the policy document for each quote. Some exclude “pre-existing conditions” (work your dentist already said you need), or only cover orthodontics for children under 19.[1][4]

- Lifetime maximums for ortho: Most plans cap orthodontic benefits at $1,000-$2,000 for life, not per year. If braces are $6,000, you’ll pay the rest.

- Annual maximums: Plans with $1,000 annual limits won’t help much with implants or multiple crowns—look for $2,000+ if possible.

- Network and copays: PPOs let you pick any dentist but pay less in-network. HMOs (like Anthem) have lower copays but require you to stay in-network.

What Real People Regret (and How to Avoid It)

- Signing up for a plan with a 12-month wait for major work—then needing a crown in month two.

- Choosing a plan that excludes implants or adult braces when that’s exactly what they need.

- Not factoring in the annual max—having coverage run out mid-treatment.

Step 3: Calculate Your Real 2- or 3-Year Cost

This is where most people miss out: Don’t just look at monthly premium. Add up:

- Total premiums paid over 2-3 years (since major work often spans years)

- Deductibles and copays for each procedure

- Out-of-pocket costs above annual and lifetime maximums

Example: You pay $70/month for a plan with a $1,500 annual max. You need an implant ($4,000) and a crown ($1,200). The plan pays 50%, max $1,500/year. You’ll cover the rest—potentially thousands more out-of-pocket. But a plan with a $5,000 annual max and no waiting period might save you far more, even if it costs $20/month extra.

Pro Tips to Outsmart the System

- Ask your dentist for codes. Get a treatment plan with procedure codes (like D6010 for implants) so you can compare coverage on what you actually need.

- Compare discounts vs. insurance. For big procedures and short timelines, a dental discount plan (like those from Aetna or Cigna) may offer bigger savings if insurance waiting periods would block coverage.[1][3][6]

- Bundle if you need vision too. Some Cigna and Spirit plans bundle dental/vision for a price break.

- Check for promotions and enrollment windows. Some insurers offer discounts or waive waiting periods if you enroll during special windows or through certain online brokers.

Urgency Alert: Don’t Wait Until Open Enrollment

Unlike medical insurance, you can buy dental insurance anytime. But the longer you wait, the more likely you’ll hit a waiting period or a coverage cutoff for pre-existing work. Act before you start treatment—once your dentist begins, many plans won’t cover that tooth.

Expert Insights: Where the Smart Money’s Going in 2025

- Spirit Dental’s $5,000 max and no waiting period is getting rave reviews from people with big treatment plans. Price: $40-$90/month.[1]

- Delta Dental PPO remains the network king—especially if you travel or want a trusted name. But check which plans actually cover implants and adult ortho.[1][7]

- Cigna’s Dental 1500 is a balanced pick if you can wait out the 12 months for ortho/major work.

- Anthem Dental HMO is a top value for Californians who want no annual max and predictable copays.[2]

Immediate Action Steps (Before You Get That Quote)

- Make a list of the major procedures you or your family will need in the next 2-3 years.

- Get pre-treatment estimates from your dentist (with codes).

- Use comparison tools on Spirit Dental, Delta Dental, Cigna, Anthem, and online brokers—filter for plans with your procedure covered, high annual max, low/no waiting period.

- Read the Summary of Benefits (not just marketing copy) before you buy.

- Calculate total multi-year costs, not just premiums.

Bottom line: If you know big work is coming, don’t gamble on the cheapest premium. Price anchor yourself to what the real cost of your care will be, and act before the clock (or your dentist’s drill) starts ticking. The right coverage now could save you thousands—and a ton of stress—down the road.