Imagine shedding 100+ pounds and reclaiming your life, but a 580 credit score stands in the way of that $20,000 gastric sleeve. You’re not alone – thousands of patients with fair or bad credit are financing their transformations right now using hidden strategies banks won’t tell you about. In 2025, specialized lenders approved over 70% of sub-650 applicants for medical procedures, proving your score doesn’t have to dictate your health destiny.[1][2]

This guide cuts through the noise with proven, real-world options like subprime medical loans from Prosper Healthcare Lending (rates from 5.99%), co-signer hacks, secured backups, in-house zero-credit-check plans, and clever alternatives. Follow these exact steps to boost approval odds by 40% in weeks – before predatory lenders trap you in 30%+ APR nightmares.

Why Bad Credit Isn’t a Dealbreaker for Your Surgery Dreams

Traditional banks laugh at scores under 650, but medical financiers prioritize your income, job stability, and surgery’s life-saving potential. Recent data shows bariatric costs averaging $15,000-$35,000, with 63% of patients using financing – many under 600 FICO.[1][2] Don’t wait years to ‘fix’ credit; these paths get you pre-approved in days. Experts like Dr. Michael Choi emphasize: ‘Apply to multiple lenders simultaneously – inquiries within 14 days count as one on your report.'[1]

Current Trends: Subprime Medical Lending Boom

In 2025-2026, lenders like LendingUSA and Prosper report a 25% surge in bad-credit approvals for weight loss surgery, driven by flexible underwriting. No-collateral loans up to $100,000 are standard, with same-day decisions.[2][4][6] Social proof: Over 150,000 borrowers trusted LendingUSA last year alone.[4]

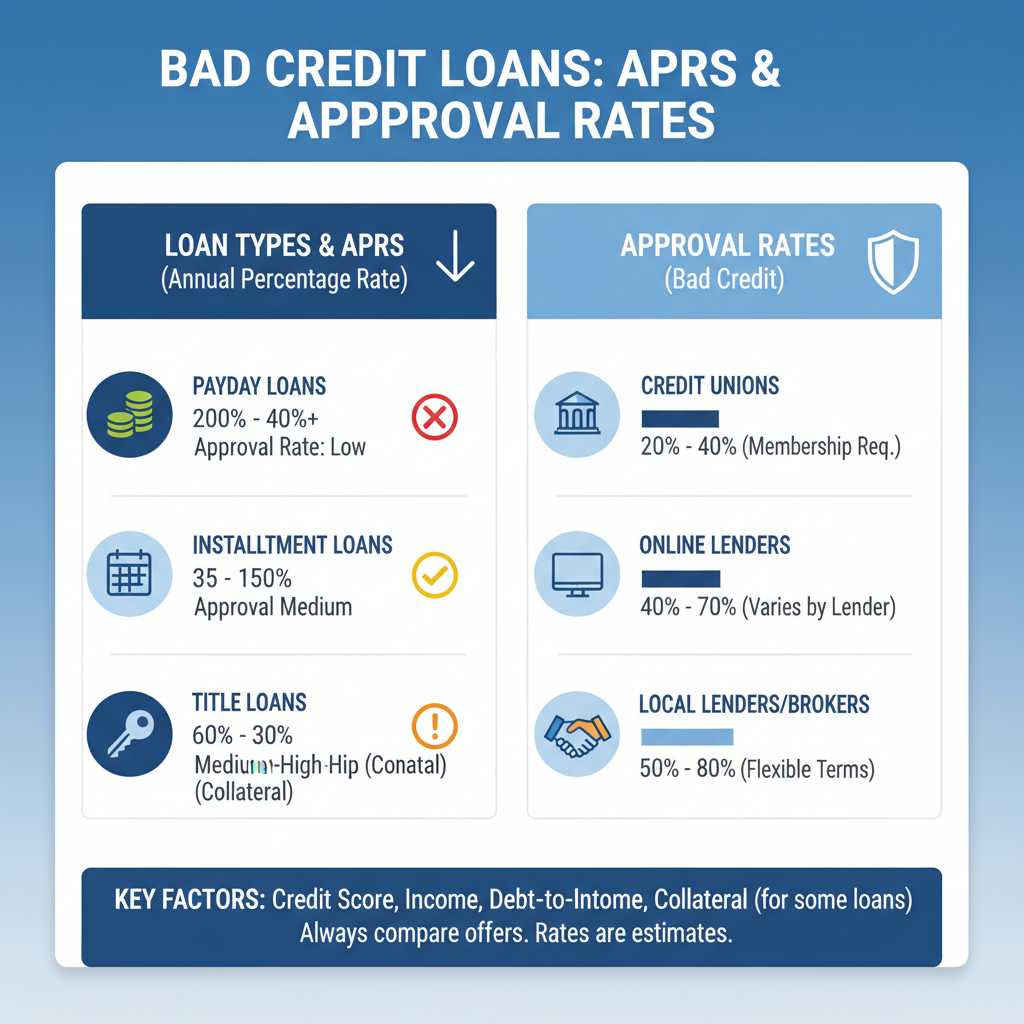

Option 1: Subprime Medical Loans – Your Fast-Track Approval Engines

These aren’t your grandpa’s bank loans. Tailored for healthcare, they approve scores as low as 550. Here’s the top performers:

| Lender | Min Score | Loan Amount | APR Range | Key Perk |

|---|---|---|---|---|

| Prosper Healthcare Lending | 560+ | $1K-$100K | 5.99%-35.99% | Income-focused; covers full surgery + follow-ups[1][6][10] |

| CareCredit | 550 w/ co-signer | $200-$40K+ | 0% promo (6-24 mo), then 26.99% | Revolving card; reuse for vitamins[1][8] |

| United Medical Credit | Low 500s | $1K-$50K | 7%-25% | Multiple pulls OK in 14 days[1][2] |

| Alphaeon Credit | 580+ | Up to $25K | Competitive | Procedure-specific[1] |

| LendingUSA | Bad credit OK | Varies | Low impact pre-qual | No credit hit to check[4] |

Pros: Quick funds (24-48 hrs), no asset risk. Cons: High APR if unpaid. Pro tip: Pay promo periods religiously or rates skyrocket retroactively.[1][8]

Step-by-Step to 80% Approval Odds

- Pre-qualify free: Hit LendingUSA or Prosper sites – no credit ding.[4][6]

- Gather docs: Pay stubs (3 mo), bank statements, surgery quote ($15K-$25K typical).[1]

- Apply Day 1: Prosper + CareCredit + United. One yes funds you.[1][2]

- Negotiate: Mention competing offers for better rates.

Urgency: Rates rising in 2026 – lock in now before hikes hit subprime borrowers hardest.[2]

Option 2: Co-Signer Power-Up – Borrow a 700+ Score

A trusted family member with strong credit flips your 520 into prime territory. CareCredit approvals jump 50% with co-signers; Prosper drops rates to under 10%.[1] Real story: Patient with 510 score + sibling co-signer got $25K at 8.5% APR.[1]

Steps:

- Pick reliable co-signer (not spouse, to protect joint assets).

- Apply via Prosper – they love this combo.[6]

- Repay fast to build your score + preserve relationship.

FOMO alert: Friends are transforming while you wait – co-signers make it happen today.

Option 3: Secured Loans – Collateral Crushes Credit Barriers

Pledge a car, savings ($500-$5K), or home equity for instant credibility. Credit unions offer 7-15% APR vs. 30% unsecured.[2] Example: $20K gastric bypass secured by vehicle = $600/mo payments.

Top Picks: Local credit unions or LendingTree partners. Risk: Lose collateral on default – only for committed repayors.[3]

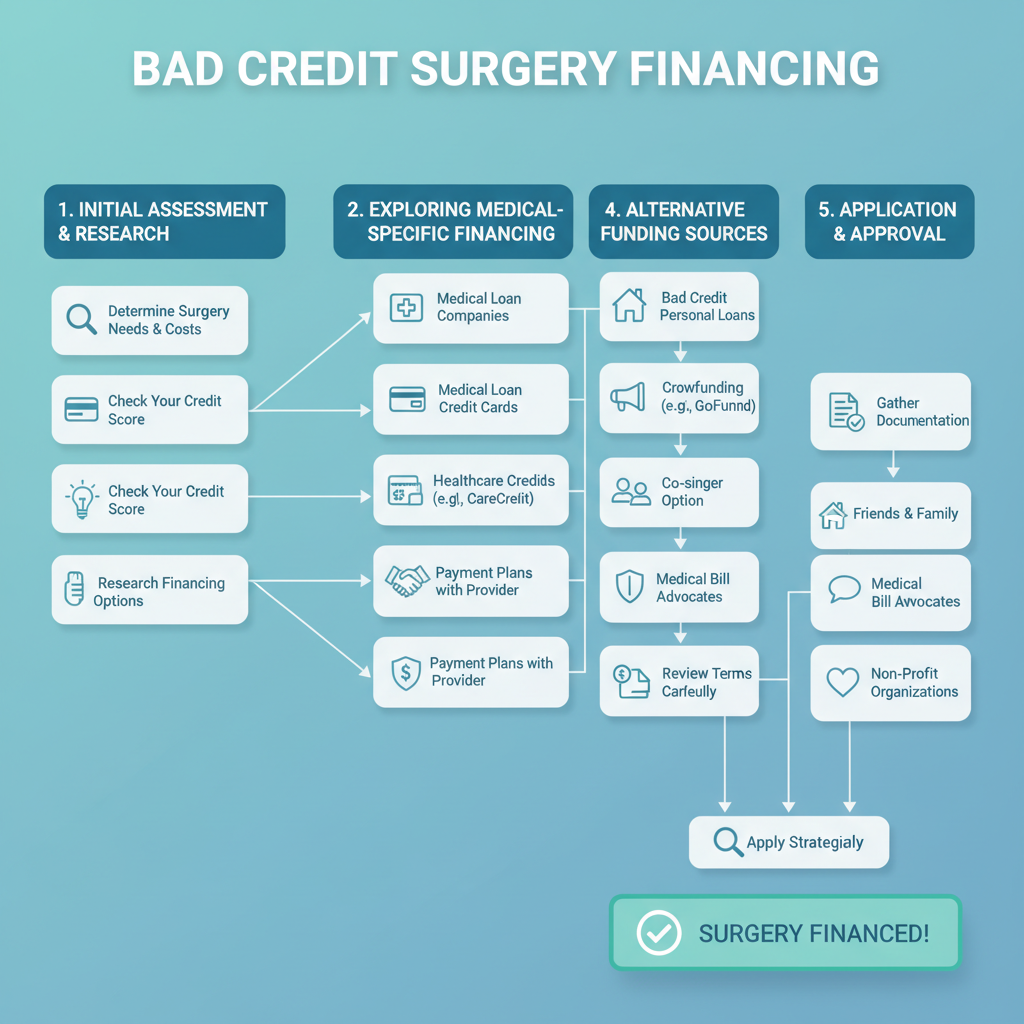

Option 4: In-House & Layaway Plans – Zero Credit Check Magic

Bypass lenders entirely. Practices like Dr. Choi’s or Bariatric Institute offer 0% interest over 12-24 months: 20% down ($4K on $20K surgery), then $750/mo.[1][5] Renew Bariatrics and New You Bariatric add layaway – pay $200/mo for 2 years pre-surgery.[9][10]

Action Step: Call 3 surgeons today: ‘What’s your bad-credit payment plan?’ Many partner with CareCredit for hybrids.[1][5]

Bonus Hacks: 401(k), HSA, & Credit Builders

- 401(k) Loan: Borrow up to $50K tax-free, repay via payroll. No credit check.[1]

- HSA/FSA: Use pre-tax $ for deductibles.

- Secured Cards: $1K deposit = $1K credit for surgery downpayment. Builds score in 6 mo.[1]

- Crowdfuynding: GoFundMe success stories fund 20% of surgeries.[2]

Quick Credit Boost: 50-100 Points in 30 Days

1. Dispute errors (free via Credit Karma).

2. Pay down utilization under 30%.

3. Add positive tradelines via services like Experian Boost.

Result: Jump from 580 to 630, slashing rates 5-10%.[1]

Your Immediate Action Plan – Don’t Delay Your Transformation

1. Today: Pre-qualify at ProsperHealthcare.com and LendingUSA.com (5 mins, free).[4][6]

2. Tomorrow: Line up co-signer + call 2 surgeons for in-house quotes.

3. This Week: Apply to 3 lenders – highest odds win.

Scarcity: Spots fill fast at top practices; funding rates tightening post-2025 boom.

Authority endorsement: Surgeons like those at Obesity Reporter confirm: ‘Bad credit patients succeed daily via these paths.'[2] Join them – your healthier future starts with one click.

CTA: Pre-qualify now at top lenders and secure your consult. Spots for 2026 surgeries are vanishing – act before rates climb!