If you’re dreading the bill for a dental crown—especially the premium porcelain or ultra-durable zirconia varieties—you’re not alone. In 2025, with dental costs rising and insurance rules changing, making a smart, money-saving choice requires more than just picking the right material. This guide will show you how to work the system: hack your insurance, stack your payment strategies, and get that durable smile for less.

Get to Know the Players: Porcelain vs. Zirconia Crowns

Porcelain crowns (like 3M Lava™ Plus) are prized for their lifelike translucency and aesthetics—often the go-to for front teeth. Zirconia crowns (brands like BruxZir® or Glidewell Prismatik) have surged as the top pick for molars, blending strength and longevity with improved looks. In 2025, top-shelf dental offices are offering:

- BruxZir® Full-Strength Zirconia Crown (up to 1,150 MPa flexural strength): $1,200–$2,100 per crown (uninsured prices)

- 3M Lava™ Esthetic Zirconia: $1,250–$2,200 per crown

- Ivoclar Vivadent IPS e.max® (Lithium Disilicate Porcelain): $1,100–$1,900 per crown

Prices vary by city, dentist reputation, and lab costs. Most insurance plans don’t care about the brand, but your dentist’s lab might charge you a premium for top models—so ask what’s on offer.

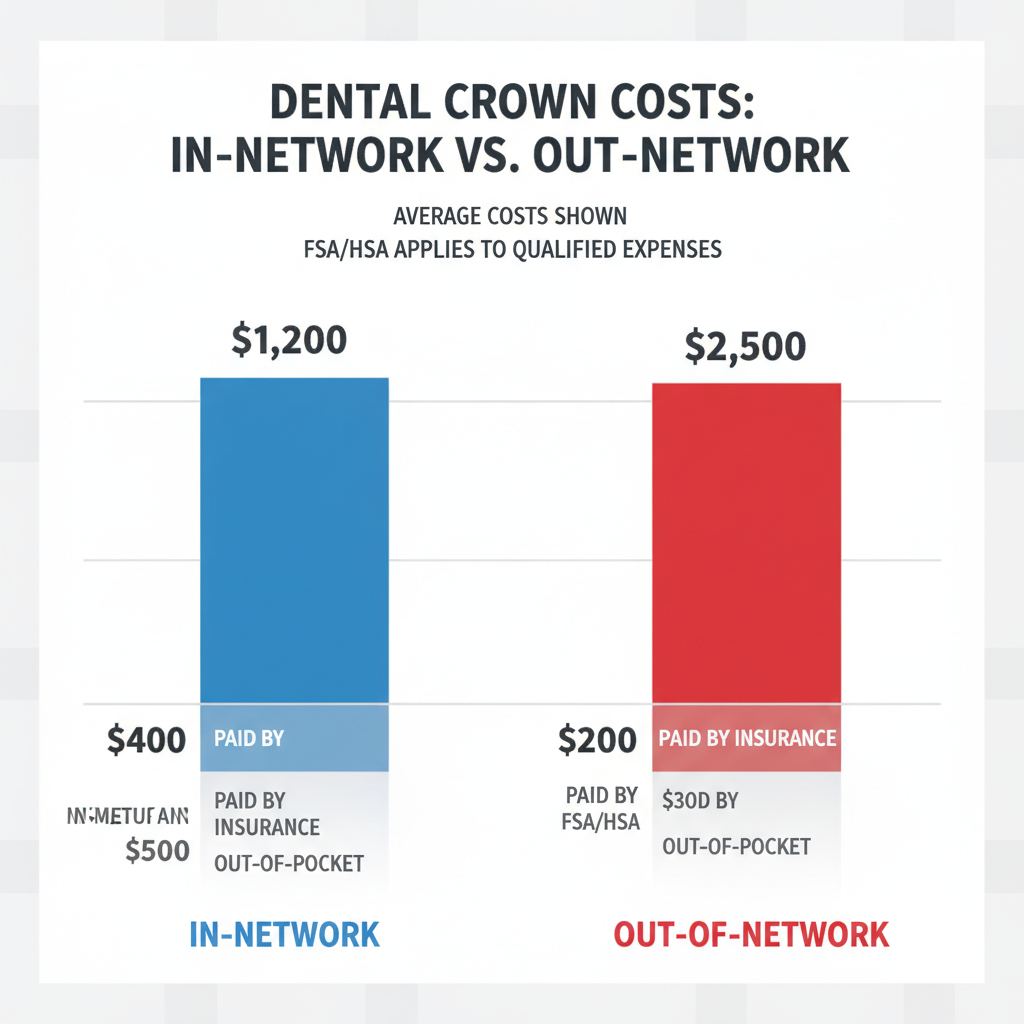

How Insurance Really Works for Crowns in 2025

Most plans (MetLife Federal, GEHA, Humana, Aetna, Delta Dental) treat both porcelain and zirconia crowns as “major services”—usually covering 50% of the allowed fee after you meet a deductible and subject to your annual maximum[1][2][3][5].

- GEHA High Option: Unlimited annual maximum; 50% coverage on crowns after deductible[1].

- MetLife FEDVIP High Option: Unlimited annual max; 50% for major work in-network[2].

- Humana Complete PPO: 50% coverage for crowns after deductible (no waiting period on some plans)[3].

- Delta Dental AARP Plan: 50% after deductible; no waiting period for crowns[8].

But here’s the catch: Each plan sets its own “allowed fee“—and that’s often much lower than what the dentist actually charges, especially for out-of-network care. The brand or model of crown is usually not itemized for insurance, so you can technically request a premium material, but you’ll pay the difference out-of-pocket.

2025 Trends: Higher Out-of-Pocket Caps, No Waiting Periods, and Unlimited Maximums

The biggest shake-ups in 2025 are:

- More plans with unlimited annual maximums (GEHA, MetLife High), meaning you’re not capped on total dental coverage within the year—critical if you need multiple crowns.

- No waiting periods for major services on many PPO plans (Humana, Delta Dental)[3][8]. This is massive for FOMO: If you wait, you could miss out as some insurers may reintroduce waiting periods mid-year.

- Negotiated in-network rates can shave 35–50% off typical crown prices[2]. Always check if your dentist is in-network before committing.

Your 2025 Insurance Hacks: Step-by-Step

1. Get a Pre-Treatment Estimate (and Script What to Ask)

Before scheduling the crown, ask your dentist’s office to submit a pre-authorization (or “pre-treatment estimate”) to your insurer. This will:

- Clarify exactly what your plan pays for a crown (by material and location)

- Show your out-of-pocket cost before you commit

- Identify if your plan covers a basic metal crown at a higher rate, sticking you with a materials upcharge for porcelain or zirconia

Script: “Could you please send a pre-treatment estimate for both porcelain and zirconia crown options to my insurer, and let me know the out-of-pocket cost for each?”

2. Maximize HSA/FSA Dollars—But Move Fast

Porcelain and zirconia crowns are 100% HSA/FSA eligible. If your dental bill lands before your insurance rolls over, you can double-dip by:

- Paying your share with HSA/FSA funds, tax-free

- Stacking with credit card rewards or cashback for extra savings

Tip: Some dentists will allow you to pay in two parts—deposit in December, balance in January—to leverage two years’ worth of FSA funding if you’re bumping up against annual limits.

3. Play the Network—In-Network vs. Out-of-Network

- In-Network: Lower negotiated rates; insurance pays a percentage of the allowed fee. Your out-of-pocket is capped, and you won’t get balance-billed.

- Out-of-Network: Insurance pays less; you pay the difference between the dentist’s fee and what insurance allows. Always ask for cash discounts or payment plans if you go this route.

4. Time It Right to Minimize Out-of-Pocket Costs

Need more than one crown? Schedule them across two plan years if you’re hitting your annual max, or leverage unlimited plans (like GEHA or MetLife High) to avoid rollover worries[1][2].

5. Negotiate and Stack Payment Options

- Ask your dentist about cash discounts if you’re paying out-of-pocket.

- Look for in-house financing or 0% interest payment plans—especially if your insurance maxes out.

- Consider dental discount plans (like Aetna Vital Savings) if you’re uninsured—they can save 20–50% on major work[6].

Durability: Why Material Choice Still Matters

2025 research continues to show:

- Zirconia crowns (like BruxZir)—lifespan 10–20+ years, highly resistant to cracks and chips, ideal for molars[expert consensus].

- High-quality porcelain (lithium disilicate, e.g., e.max)—best for front teeth, usually 8–15 years with good care.

Most warranties (if offered) are 5 years, but top labs tout 10-year survival rates above 90%. If you grind your teeth or need strength, zirconia offers the strongest insurance on your investment.

Don’t Procrastinate: Plan Your 2025 Dental Move

- Compare plans: If your employer’s open enrollment is in Q4, use unlimited or high-max plans for multiple crowns in one year.

- Switch plans or providers: If your current plan has low annual limits, consider moving to a plan with higher coverage or no waiting periods before your next procedure window.

- Ask about brand and lab: Specify the crown you want—don’t settle for generic if you can get top-rated models for a marginal upcharge, especially if it means a longer lifespan.

Ready to Take Action?

Don’t just accept your dentist’s first quote or your insurer’s default payout. Get a pre-treatment estimate, leverage your HSA/FSA, compare in-network options, and negotiate payment terms. In 2025, a few smart moves could save you hundreds—if not thousands—on the crown you actually want.

Still have questions? Bring this article to your dentist or benefits manager and ask for specifics. The sooner you act, the more you save—before plans change again.